Mounting public pressure on brand owners and retailers to reduce the environmental impact of packaging is one of the biggest challenges facing rigid plastic packaging producers over the next five years. Measures being introduced by governments and brand owners/retail chains to lower consumption of non-renewable and non-recyclable packaging materials are part of a growing focus on sustainability.

The Future of Rigid Plastic Packaging to 2026, a new report from Smithers, identifies consumption of the material in 2020 as 58.83 million tonnes with only a marginal increase in demand during the year due to severe disruption by the COVID-19 pandemic. As recovery takes place, total market value will reach $193.2 billion in 2021, up from the $181.9 billion seen in 2020 for a 6.2% increase.

Beyond 2021 a compound annual growth rate (CAGR) of 4.2% will push the global market to $237.1 billion in 2026 with Asia leading the rise in consumption. Total volume consumption worldwide will rise by 3.5% across 2021-2026 to reach 73.1 million tonnes, Smithers data shows.

Sustainability initiatives

New product developments for rigid plastic packaging are focused mainly on sustainability and the circular economy. There are further developments in PET food-grade resin with recycled content and growing uptake of recycled PET for packaging. Paper bottles are gaining traction but are unlikely to make a major breakthrough into mainstream packaging markets in the foreseeable future.

Chemical recycling

Another growing area involving sustainability is chemical recycling, which may offer the potential for difficult-to-recycle PET and other polymer streams in the future as a supplement to mechanical recycling. Chemical recycling involves reducing waste PET and other plastic packaging to its constituent parts or chemical feedstock. Recent chemical recycling technology developments could be a ‘game changer’ for PET and other packaging polymers.

Several projects for chemical recycling of waste PET and other plastic packaging currently under development. By 2026, chemical recycling could potentially break down difficult-to-recycle plastic packaging waste. However, the challenge is whether the industry can develop the technologies to a scale that is both industrially and economically feasible.

Regional growth potential

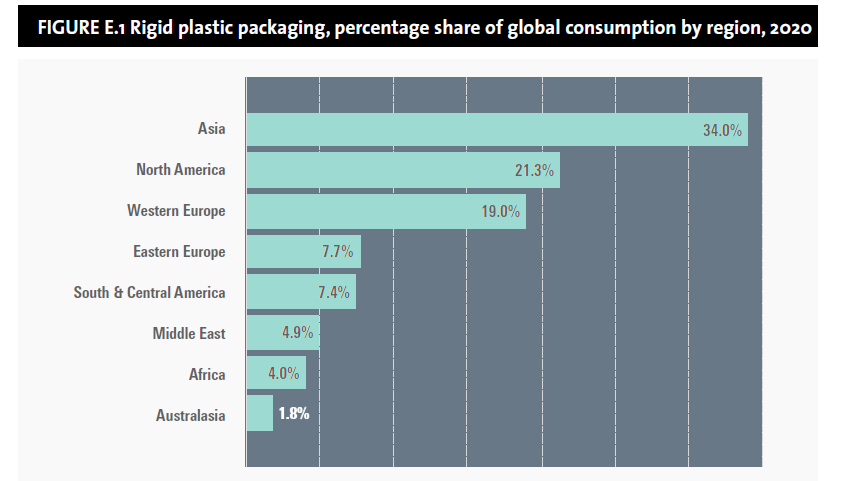

In 2020, Asia was the largest consumer of rigid plastic packaging with consumption share of 34.0%, followed by North America with 21.3% and Western Europe with 19.0%. Asia is forecast to grow rigid plastic packaging consumption during 2021–26 at the fastest rate, with high growth rates in India and China being propelled by rising standards of living, growing urbanisation and wider availability of packaged food and drink. Japan is a highly developed and mature market and rigid plastic packaging consumption is forecast to grow quite slowly.

Africa and the Middle East are forecast to grow rigid plastic packaging at rates above the global market average rate. Packaging markets in most countries in Africa and the Middle East are relatively under-developed and offer good growth potential. Rigid plastic packaging consumption is rising as a result of a young and growing population, increased urbanization and expansion of a wealthier middle class, investment in food production, food processing and new packaging converting capacity, and the development of a more modern retail infrastructure along with increased use of pre-packed foods.

With growing demand for convenience food as a part of Asia’s urbanization, rigid plastic package makers can expect to see higher sales of microwavable ready meals in thermoformed rigid plastic packages, more portable packaging, ‘easy-open’ and reseal packaging and packaging for on-the-go lifestyles.

Western Europe and North America are very mature and saturated markets for rigid plastic packaging with high penetration rates across various end-use sectors. Furthermore, consumers’ real disposable incomes and the population are growing at a relatively modest rate.

Source: Smithers

Leading applications

Source: Smithers

Leading applications

Food is the largest end-use market for rigid plastic packaging, accounting for 40.0% of global consumption in 2020. Within the food category, dairy products are by far the largest sector, followed by other (human) foods, which include soups, sauces, seasonings and condiments. Non-food is the second largest sector, representing 31.9% of

consumption, followed by drinks with a 28.1% consumption share. Other (human) food is forecast to grow at the highest rate, followed by healthcare and cosmetics.

Leading processes

Blow molding is the most important process used for the manufacture of rigid plastic packaging, accounting for 59.6% of global consumption in 2020, followed by injection molding with 17.6%. Thermoforming accounts for 15.1% of consumption and thermoform-fill-seal has a 7.1% share.

The thermoform-fill-seal rigid plastic packaging process is forecast to grow at the fastest rate, mainly as a result of growing demand for single-serve packs and the versatility and speed of the machinery that enables rapid changeovers to ensure optimum productivity of operations.