Market Report

The Future of Spunlace Nonwovens to 2024

The latest research from Smithers identifies market challenges for spunlace nonwovens in four major end-use markets.

Exclusive data from the Smithers study - The Future of Spunlace Nonwovens to 2024 - shows that in 2019, spunlace will account for 12.1% off all nonwovens consumed. Consumption is projected to be 1.4 million tonnes or 31.1 billion square metres in 2019, with a global value of $6.19 billion.

Most significantly spunlace formulations represent the fastest growing of all non-woven material formats. Growth by tonnage is forecast to increase at 7.9% year-on-year to exceed 2 million tonnes in 2024. Value will rise at a slightly faster rate to reach $9.15 billion in that year.

Spunlace nonwovens are employed in both disposable and durable non-woven products. In general disposable spunlace products have seen stronger growth since 2014, as these are mass-market applications, such as baby wipes, and the secondary top sheet of feminine hygiene products. Disposable nonwoven products tend to be more specialised and have higher-margin than durable nonwoven products.

Growing demand for these disposable items among an emergent and aspirational middle classes in Asia make this the largest regional market for spunlace nonwovens and its largest producer. Asia has 277 identified installed spunlace lines with a capacity of about 1,070,000 tonnes in 2019. China alone has almost 200 installed lines and nameplate capacity of over 800,000 tonnes. This will underpin a further growth of Asian demand for spunlace products of nearly 350,000 tonnes through to 2024.

Future expansion and profitability in the spunlace segment will be powered by a combination of both evolution in consumer demand, cost dynamics in supply and innovations in technology. Smithers’ expert analysis identifies the following leading market trends:

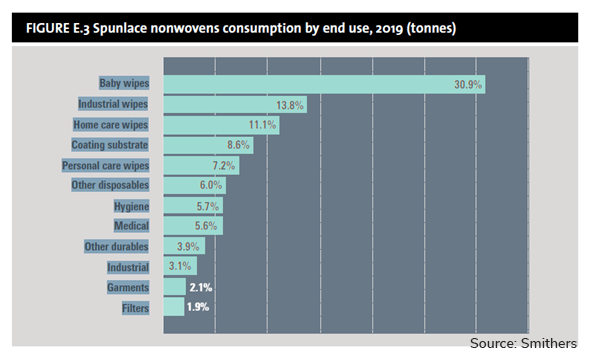

The largest end use for spunlace nonwovens is wipes. This accounts for 63.0% of all spunlace consumption in 2019, with nearly half of these being used in baby wipes.

Nonwovens used in baby wipes are mainly spunlace due to their strength and softness, an in spite of their being expensive and not fully biodegradable.

Three recent innovations in baby wipes globally are:

The next fibre innovation in baby wipes may be nonwovens made from bio-based polymers Producers are trialling a spunlace made from polylactic acid (PLA) and negotiating better and more consistent pricing for PLA fibre.

The recent boom in demand for wipes has created an oversupply of high-performance, lower-cost dispersible spunlace nonwovens for flushable wipes – a market once limited by the availability of viable dispersible nonwoven substrates. At least nine new nonwovens production lines entered service between 2013 and 2019 using new technologies for the flushable nonwovens wipes market.

Consequently flushable wipe producers are looking to new flushable wipe markets. The principle technical target is to evolve contemporary technology to improve dispersibility and increase flushability. If a product can be designed with equivalent flushability to toilet tissue, then potential issues with both the wastewater industry and government regulatory agencies will be avoided.

Hygiene is a relatively new market for spunlace. The main applications are in stretch ears for diapers/nappies and the secondary top sheet for feminine hygiene products. It penetration has been restrained by production and cost considerations compared to spunlaid manufacture.

Sustainability is growing in importance for disposable items. The European Union agreed its Directive on Single-Use Plastics, on December 2018. Sanitary napkins are one hygiene product on its initial target list. Hygiene product producers are also keen for more sustainable products that they can sell to consumers concerned about the environment, although price will continue to be an equally important factor to 2024.

There is an impetus on all market participants to contribute towards this goal:

The first major market for spunlace was in medical applications including surgical drapes, surgical gowns, CSR wrap, and wound dressings. Many of these end-uses have now been taken over by spunlaid nonwovens, however.

Spunlace is unlikely to match the cost of spunlaid nonwovens in this end use; buyers of medical nonwovens who value performance and sustainability must be identified and engaged. To increase spunlace use in medical products, raw material suppliers must identify and supply low-cost, sustainable raw materials that are absorbent and offer structures with higher strength and stretch than current spunlace products.

The implications of these trends on future production and profitability is analysed in detail the Smithers Study - The Future of Spunlace Nonwovens to 2024 - and quantified in over 120 data tables and figures.